UPS Q1 2026 Earnings: Key Takeaways for Shippers

UPS’s Q1 2026 earnings call didn’t deliver the same headline strength as FedEx’s recent quarter, but in many ways it confirmed the same message:

The parcel market isn’t reverting to its old model. It’s continuing to evolve into something structurally different.

For shippers, that shift has real implications.

UPS Is Proving You Don’t Need More Volume to Make More Money

The clearest signal from the Q1 2026 UPS earnings call was how comfortable UPS is operating with less volume.

U.S. Domestic Segment revenue declined 2.3%, driven by an expected decline in volume, in part from the ongoing reduction of Amazon volume and a deliberate exit from lower-margin e-commerce shipments. At the same time, revenue per piece increased 6.5%, allowing UPS to offset much of that decline.

UPS is no longer optimizing for scale. It is optimizing for profitability per shipment.

That distinction matters. For years, shippers could rely on volume as leverage. The more you shipped, the more valuable you were to the carrier network. That assumption is weakening.

Not All Shippers Are Equal Anymore

UPS was explicit about where it sees growth:

- Small and mid-sized businesses

- B2B shipments

- Healthcare, including direct-to-consumer pharma

Healthcare alone generated its first-ever $3 billion quarter for UPS, with executives calling out GLP-1 drugs and other time- and temperature-sensitive shipments as key drivers of future growth. These high-value segments command higher pricing and more consistent margins.

At the same time, UPS confirmed it has been actively removing lower-yielding e-commerce volume from its network, including international and China-linked traffic, and “making that volume available to the market.”

The Economy Lane Is Getting More Expensive

One of the more telling comments during UPS’s Q1 earnings call came in response to a question about USPS pricing.

UPS noted that when USPS raises prices, it effectively raises the floor for economy shipping across the industry, and called that “good for the market.”

For shippers, the implication is straightforward: there is no longer a reliable “low-cost fallback.”

As USPS raises rates, and as UPS and FedEx continue to push toward higher-yield customers, the entire pricing spectrum shifts upward.

This is consistent with what we’ve been tracking across the market: economy services are being repriced, restructured, or deprioritized.

Fuel Surcharges: Protection for Carriers, Risk for Shippers

UPS took a more conservative stance than FedEx on fuel surcharges, describing them as a mechanism to “protect profit” rather than generate upside, but the practical effect is the same.

Fuel volatility is passed through to shippers. However, UPS also acknowledged that sustained increases could impact demand, a subtle but important difference from FedEx’s more confident posture.

Notably, UPS did not address its newly introduced Emergency Surcharge clause on this earnings call, but its emphasis on volatility and flexibility suggests exactly why the mechanism was put in place.

A More Efficient Network Means Less Need for Low-Margin Volume

UPS is backing its pricing strategy with significant operational changes:

- Roughly 30,000 roles reduced

- 7,500 driver positions eliminated

- 50 facilities planned for closure (23 buildings this quarter with plans to close 27 more this year)

- Automation delivering materially lower cost per piece

These are not incremental optimizations. They are structural.

As the network becomes more efficient, UPS becomes less dependent on volume to maintain margins. That reinforces its ability to be selective about the freight it carries.

Tariffs Are a Pass-Through

One other notable point from the call: UPS reiterated that tariffs are a pass-through cost, remitted directly to the government.

That’s technically true, but it misses the operational reality. UPS controls the filing process, and in many cases:

- Acts as the customs broker

- Determines how entries are submitted

- Ultimately controls the timing of refunds

For more information on the IEEPA tariff refund process for UPS and FedEx, read our blog post.

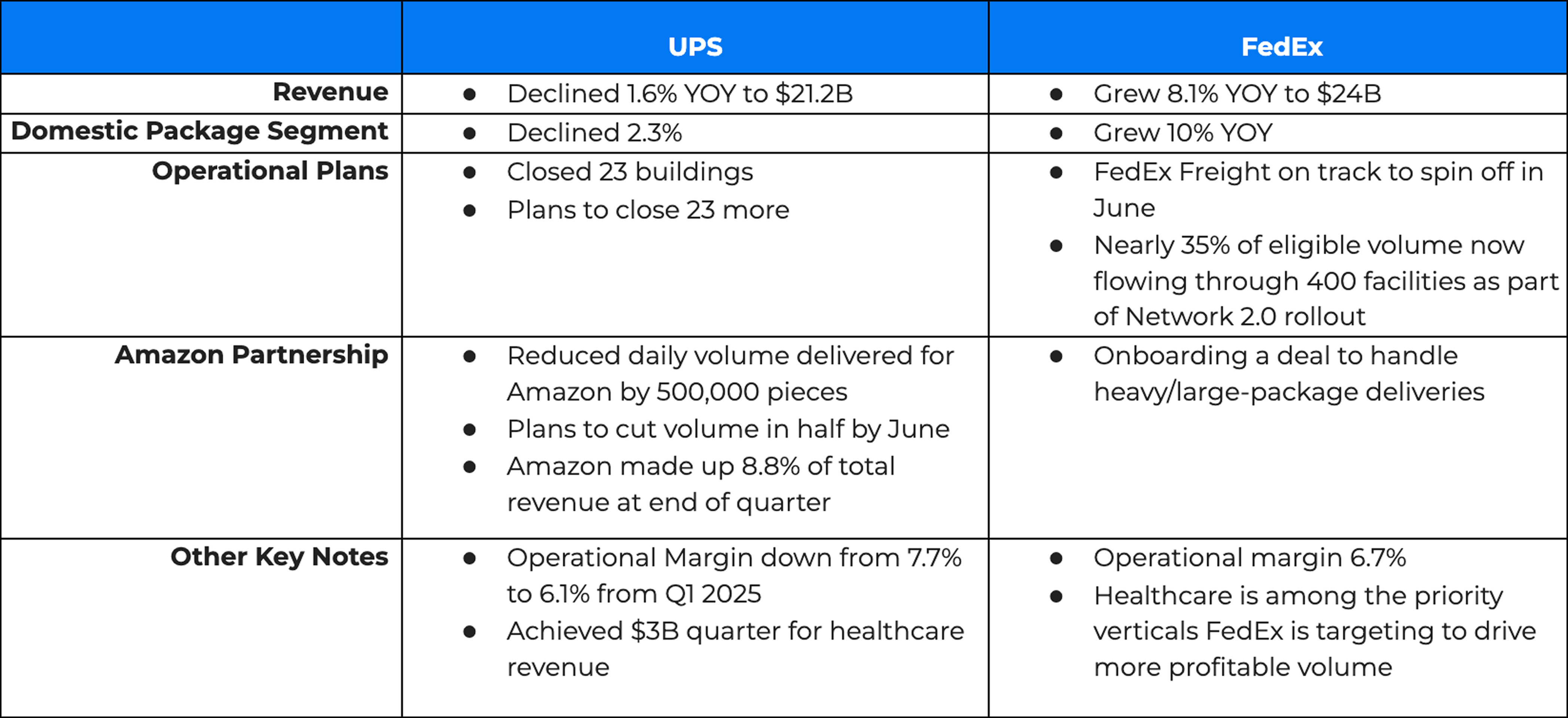

UPS versus FedEx Performance

This earnings call shows a stark contrast between current carrier performance, and was the principal driver of FedEx surpassing UPS in market capitalization this year. The table below is included for comparison based on UPS’s April earnings call and FedEx’s March earnings call.

Key Takeaways for Shippers

Taken together, signals from UPS’s Q1 2026 earnings call point to a consistent shift across the industry:

Carriers are prioritizing yield over volume, and redesigning their networks accordingly.

That creates a different operating environment for shippers. The question for shippers is no longer how to secure the lowest rate. It’s how to operate within a system where:

- Pricing is becoming more volatile

- Carrier priorities are shifting

- Not all volume is created equal

- The economy floor is being pushed upward

This environment requires a more active approach to carrier strategy, contract structure, and network design.

Will shippers still have leverage in this evolution of the parcel shipping market?

Yes.

However, the gap between “winners” and those left behind will continue to increase as companies of all sizes must actively rethink the role shipping strategy plays in the overall health of their businesses.

Access This Content

Change the Economics of Your Shipping

Better Rates.

Complete Visibility.

Strategic Edge.